Iran War and Dollar Depreciation: Can the Greenback Maintain Its Global Dominance?

The possibility of an all-out war between America and Iran has brought much discussion about whether or not the US dollar will remain world's dominant reserve currency. History has shown that safe-haven currencies always benefit in the short term from military conflict. If a confrontation with Iran were to be drawn out, however, those same trends undermining dollar supremacy could be further accelerated.

Immediate Market Reactions

In the event of open hostilities, initial market behavior would likely follow established patterns. The dollar typically strengthens during geopolitical crises as investors flee to safety. Treasury bonds would see increased demand, and dollar-denominated assets would temporarily benefit from global risk aversion. However, this conventional wisdom assumes limited duration and contained scope—assumptions that may not hold in a conflict with Iran.

The Islamic Republic is home to a series of asymmetric capacities, among them the potential to cut off the flow of oil to world markets through the strait of Hormuz, where about 20% of international oil passes. If the channel is blocked for any length of time (and this could prove to be quite possible anywhere); then what appears as a positive earthquake on the currency markets will in fact help reduce real income everywhere that supports its value--a cruel irony indeed.

Structural Threats to Dollar Hegemony

If the conflict were protracted, then existing threats to dollar dominance would intensify. First, military outlays would exacerbate America’s already unsustainable public finance trajectory. With debt levels topping 120% of GDP, war funding through more borrowing could deepen doubts about long-run solvency and potentially trigger credit rating downgrades.

Secondly, sanctions--Washington's favorite instrument of financial warfare--would see declining returns. Extensive sanctions on Iran have already led targeted countries to travel in the direction of alternative payment systems. A major war would presumably prompt fresh sanctions regimes, driving more states not to breaching penalties but via bilateral currency swaps and systems of non-dollar settlement. Russia, China, and India have each built dedicated routes for avoiding dollar denominated transactions.

The Geopolitical Realignment

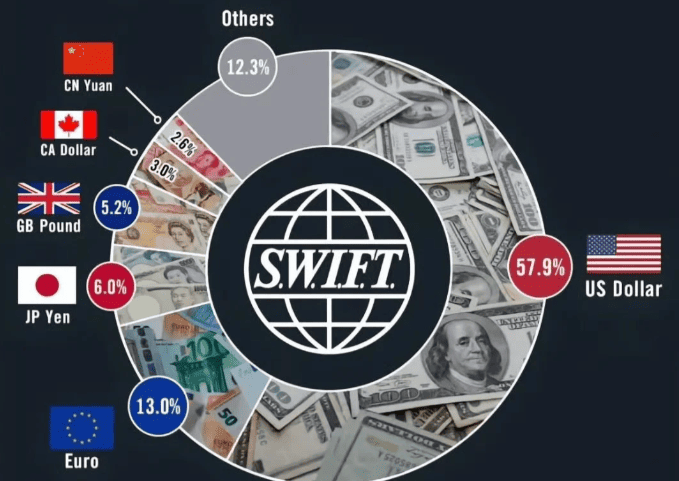

US-Iran war would be a critical tipping point for the global economic order. Regional powers will come under intense pressure to take sides, and many will be looking for ways to limit their vulnerability to America's financial control. The weaponization of the dollar payment infrastructure (SWIFT, correspondent banking relationships, clearing systems) has already shown that if you rely on dollar settlement, you become politically vulnerable.

China's digital yuan, broader BRICS pay methods, as well as local-currency trading agreements between nations are the early stages of this movement. Across major energy-exporting countries that are not essentially in lockstep with Washington, a significant Middle Eastern conflict could serve both a reason and screen for deepening these trends.

Historical Precedents and Unique Risks

Past dollar crises give only limited guidance. The 1970s oil shocks resulted in a temporary weakening of the currency, but ultimately consolidated its role in commodity pricing. The financing of the 2003 invasion of Iraq through deficit spending contributed to the dollar's decline between 2002 and 2008 without displacing its reserve status.

However, current circumstances are significantly different. America's share of the global GDP has significantly declined; alternative economic centers have matured in their calculability, digital technology gives currency substitution much less friction. In contrast to all previous conflicts, a war with Iran would take place during active great power competition with China, thus reducing Washington's ability to coordinate supportive monetary policies in conjunction with allied states.

Conclusion

The US dollar will not collapse overnight. Network effects, liquid markets, institutional inertia, and the lack of credible alternatives ensure its continued dominance over the short term. The euro remains politically fragmented, the yuan lacks convertibility, while cryptocurrencies are unreliable.

An US-Iran war will not necessarily bring about a global crisis, at most it would only elevate what is an accelerating trend anyway. The dollar would remain the main reserve currency but would face much fiercer competition in trade settlement, commodity pricing and credit across borders. American leaders will have to face an unpleasant fact: the two props of exerting military power and running a financial empire, which have long worked together, are now more contradictory.